ศูนย์วิจัยเศรษฐกิจและธุรกิจ ธนาคารไทยพาณิชย์ (อีไอซี) ออกบทวิเคราะห์ เรื่อง Robo advisor โอกาสที่มาพร้อมการเปลี่ยนแปลงของภาคสถาบันการเงิน โดยระบุว่า · Robo advisor เป็น Fintech ด้านบริหารความมั่งคั่งออนไลน์ ที่รองรับความต้องการใช้บริการแนะนำการลงทุนแก่นักลงทุนทั่วไป มีจุดเด่นเรื่องต้นทุนการให้บริการที่ต่ำ และมีแนวโน้มพัฒนาไปสู่การให้บริการรอบด้านแบบสถาบันการเงินในอนาคต

· อีไอซีมองเทคโนโลยี Robo advisor เป็นโอกาสเสริมคุณภาพบริการด้านการจัดการความมั่งคั่งของสถาบันการเงิน เพื่อพัฒนาประสิทธิภาพการให้บริการ รวมถึงรักษาและขยายส่วนแบ่งตลาดในธุรกิจดังกล่าว

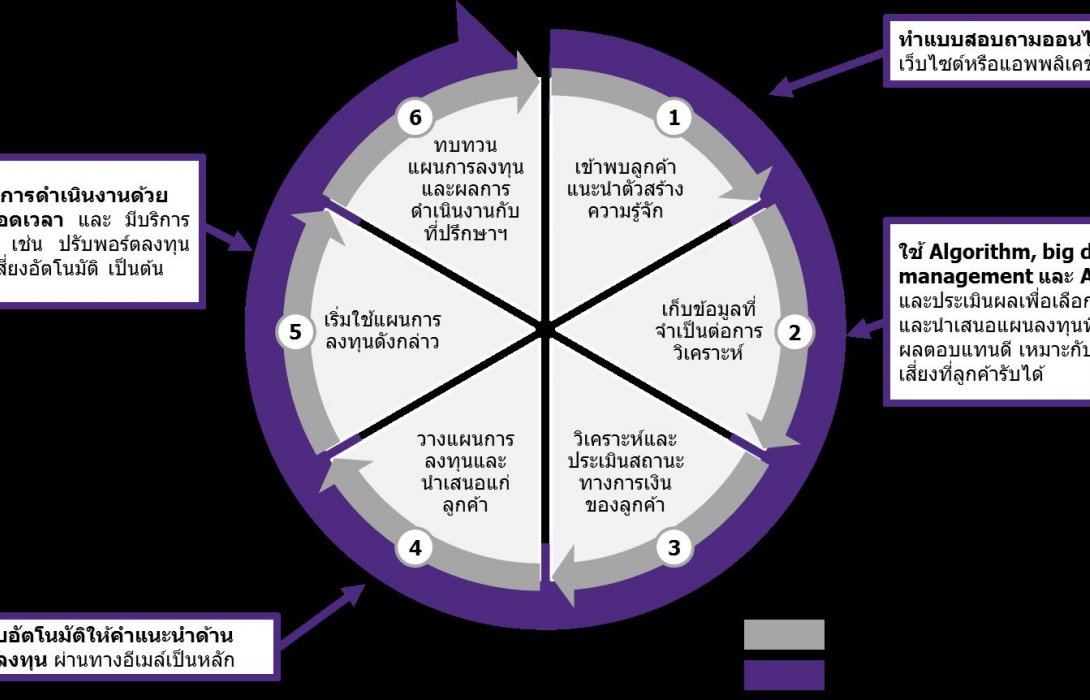

Robo advisor คือเทคโนโลยีทางการเงิน (Fintech) ที่ให้บริการแนะนำการลงทุนแบบออนไลน์แก่นักลงทุนทั่วไป การแนะนำการลงทุนเป็นบริการในหมวดบริหารความมั่งคั่ง (wealth management) ซึ่งรวมการจัดการการลงทุน (investment management) ที่ปรึกษาทางการเงิน (financial advisor) และการวางแผนทางการเงิน (financial planning) เข้าไว้ด้วยกัน โดยที่ผ่านมาเน้นให้บริการแก่กลุ่มลูกค้าที่มีความมั่งคั่งสูง (High Net Worth Individuals) ทำให้บุคคลทั่วไปเข้าถึงบริการเหล่านี้ไม่ง่ายนัก ผู้ประกอบการ startup จึงได้พัฒนาเทคโนโลยีทางการเงินที่ให้คำแนะนำด้านการลงทุนส่วนบุคคลทั่วไปขึ้นมา ซึ่งเรียกว่า Robo advisor ซึ่งประกอบด้วยอัลกอริทึม (algorithm) การจัดการข้อมูลจำนวนมาก (Big Data management) และสมองกล (Artificial Intelligence) มาใช้ร่วมกับการให้คำปรึกษาด้านการเงิน (financial advisory) เพื่อวางแผนการลงทุนในสินทรัพย์ทางการเงินประเภทต่างๆ

ด้วยบริการที่เข้าถึงคนส่วนใหญ่และมีความหลากหลาย ทำให้ Robo advisor กลายเป็น Fintech อันดับหนึ่งที่น่าจับตามองของภาคอุตสาหกรรมการเงินทั่วโลก Robo advisor ถูกพัฒนาขึ้นเพื่อทดแทนการให้คำปรึกษาด้านการออมและการลงทุนแบบตัวต่อตัว (face to face advisory) โดยมีวัตถุประสงค์เพื่อลดต้นทุนในการให้บริการการแนะนำด้านการลงทุนและบริหารความมั่งคั่งแก่บุคคลทั่วไป โดยแผนการลงทุนที่ได้รับจากการใช้บริการนี้ขึ้นอยู่กับ 1) เป้าหมายการลงทุนของผู้ใช้งานแต่ละคน เช่น การวางแผนการลงทุนเพื่อเกษียณอายุ หรือ การลงทุนเพื่อสร้างความมั่งคั่ง และ 2) ระดับความเสี่ยงที่รับได้ของผู้ใช้งานแต่ละคน นอกจากนี้ ยังสามารถปรับสมดุลพอร์ตลงทุนอัตโนมัติเพื่อป้องกันความเสี่ยง และมีบริการเสริมอื่นๆ ที่เริ่มครบวงจรมากขึ้น อาทิ ผู้ให้บริการในสหรัฐฯ มีบริการลดหย่อนภาษีเงินได้จากการลงทุน (tax loss harvesting)1 การซื้อ-ขายเศษหุ้น (fraction shares)2 รวมถึงการให้กู้ยืมเพื่อซื้อหลักทรัพย์เพื่อนำไปลงทุนต่อ (margin loans) เป็นต้น นอกจากนี้ ผู้ให้บริการอย่าง Betterment และ Charles Schwab IP ยังมีบริการเสริมแบบพรีเมียม เช่น การเข้าถึงที่ปรึกษาทางการเงินส่วนตัว เพื่อตอบโจทย์ลูกค้ากลุ่ม High Net Worth Individuals ที่ต้องการใช้บริการด้วย Robo advisor

จุดเด่นที่ทำให้ Robo advisor เป็นที่นิยมอย่างแพร่หลายในต่างประเทศ มี 3 ข้อหลัก ดังนี้ 1) ใช้เงินลงทุนแรกเริ่มน้อยกว่า ในอดีตสิ่งหนึ่งที่ทำให้บุคคลทั่วไปไม่สามารถใช้บริการแนะนำการลงทุนได้ คือ การกำหนดประเภทลูกค้าจากวงเงินขั้นต่ำ ที่พบว่าโดยเฉลี่ยคือตั้งแต่ 50,000 ดอลลาร์สหรัฐฯ ขึ้นไป ขณะที่ ผู้ให้บริการด้าน Robo advisor เช่น Betterment หรือ Acorn ไม่กำหนดวงเงินขั้นต่ำสำหรับการเริ่มใช้บริการ 2) ค่าธรรมเนียมการให้บริการรายปีถูกกว่า เฉลี่ยอยู่ที่ 0% - 0.5% ของมูลค่าสินทรัพย์ภายใต้การจัดการ (Asset Under Management) ขณะที่บริการแนะนำการลงทุนปกติอยู่ที่ 1% - 3% ของมูลค่าสินทรัพย์ฯ และอาจมีค่าธรรมเนียมอื่นๆ เพิ่มเติม และ 3) สามารถแนะนำพอร์ตลงทุนที่เหมาะสมได้อย่างรวดเร็ว เนื่องจากเป็นขั้นตอนที่ทำผ่านทางออนไลน์ได้ทั้งหมดด้วยตนเอง นอกเหนือจากนี้ ผู้ให้บริการหลายราย เช่น Wealthfront และ Assetbuilder ยังระบุสัดส่วนหน่วยลงทุนในผลิตภัณฑ์ทางการเงินประเภทต่างๆ ได้อย่างละเอียดอีกด้วย ทำให้การลงทุนผ่าน Robo advisor เป็นทางเลือกที่ได้รับความนิยมจากนักลงทุนในต่างประเทศมากขึ้น

ทว่าสถาบันการเงินรายใหญ่ของโลกยังคงเป็นเจ้าตลาดในธุรกิจแนะนำการลงทุนและบริหารความมั่งคั่ง แม้ผู้ประกอบการ startup ด้าน Robo advisor มีแนวโน้มขยายตัวต่อเนื่อง Business Insider Intelligence หน่วยงานวิจัยด้านธุรกิจ คาดการณ์ว่ามูลค่าสินทรัพย์ภายใต้การจัดการของธุรกิจ Robo advisor ทั่วโลก จะอยู่ที่ราว 8 ล้านล้านดอลลาร์สหรัฐฯ ในปี 2020 หรือกว่า 8% ของมูลค่าสินทรัพย์ภายใต้การจัดการของสถาบันการเงินทั่วโลก (รูปที่ 4) สะท้อนถึงแนวโน้มของเทคโนโลยี Robo advisor ที่เข้ามามีบทบาทกับภาคสถาบันการเงินในอนาคต อนึ่ง ข้อมูล ณ เดือนกุมภาพันธ์ ปี 2017 พบว่าผู้นำธุรกิจด้าน Robo advisor 2 อันดับแรกจาก 10 อันดับ เป็นของสถาบันการเงินด้านธุรกิจหลักทรัพย์จัดการกองทุน (บลจ.) อย่าง Vanguard PA และ Charles Schwab IP ซึ่งมีมูลค่าสินทรัพย์ภายใต้การจัดการรวมกันกว่า 74% ของทั้งหมด แสดงถึงข้อได้เปรียบเรื่องเงินทุนเพื่อพัฒนาเทคโนโลยี ฐานลูกค้าเดิม ความน่าเชื่อถือของบริษัท ตลอดจนความหลากหลายของผลิตภัณฑ์ทางการเงินของสถาบันการเงินขนาดใหญ่

ปัจจุบัน Robo advisor อยู่ในขั้นการพัฒนา แต่สามารถเพิ่มคุณภาพบริการหากนำมาใช้ร่วมกับผู้ที่ทำงานในธุรกิจที่เกี่ยวข้อง Robo advisor สามารถช่วยจัดการข้อมูลจำนวนมาก ตลอดจนประมวลผลข้อมูลจากหลายแหล่งพร้อมกันเพื่อเฟ้นหาสินทรัพย์ทางการเงินที่เหมาะสมและให้ผลตอบแทนดี ทว่าระดับการพัฒนาของเทคโนโลยีด้าน Robo advisor ในปัจจุบันยังไม่สามารถทำงานอย่างเป็นอิสระจากมนุษย์ได้ เช่น การซื้อ-ขายสินทรัพย์ทางการเงินที่ยังต้องทำผ่านนายหน้าซื้อ-ขาย หรือ การประเมินผลการดำเนินงานของระบบโดยผู้จัดการกองทุน รวมไปถึงการวิเคราะห์และให้คำแนะนำการลงทุนภายใต้เงื่อนไขของผู้ใช้งานที่มีความซับซ้อน เช่น สถานภาพ ความมั่นคงในหน้าที่การงาน หรือ ความมั่นคงทางการเงิน อีกทั้งข้อจำกัดด้านการสร้างปฏิสัมพันธ์กับลูกค้าที่ต้องใช้จิตวิทยาและความละเอียดอ่อนด้านการสื่อสาร ดังนั้น การนำ Robo advisor มาใช้ร่วมกับที่ปรึกษาการลงทุน ผู้ที่เกี่ยวข้องในธุรกิจบริหารความมั่งคั่ง และธุรกิจแนะนำการลงทุนจึงสามารถเสริมศักยภาพการให้บริการได้ดียิ่งขึ้น

นักลงทุนทั่วไปในไทยมีความสนใจที่จะลงทุนด้วย Robo advisor นักลงทุนทั่วไปมีแนวโน้มใช้ช่องทางออนไลน์เพื่อลงทุนมากขึ้น โดยเฉพาะการซื้อ-ขายหลักทรัพย์ออนไลน์ที่มีการขยายตัวต่อเนื่องราว 30% จากในอดีต ทั้งนี้ ผลสำรวจจาก Accenture บริษัทให้คำปรึกษาด้านการจัดการ พบว่ากว่า 94% ของผู้ตอบแบบสอบถามชาวไทยที่ใช้บริการธนาคารดิจิทัล มีความพร้อมในการใช้เทคโนโลยี Robo advisor เพื่อจัดการการลงทุนส่วนบุคคล แต่เทคโนโลยีดังกล่าวยังไม่เป็นที่รู้จักอย่างแพร่หลายนัก อีกทั้งบริการที่มีในประเทศยังคงจำกัดเพียงเฉพาะกลุ่มลูกค้า High Net Worth Individuals เท่านั้น

ผู้ที่จะให้บริการด้าน Robo advisor ในไทยต้องผ่านการทดสอบ Regulatory Sandbox ก่อนเริ่มใช้จริง ผู้ประกอบการทั้งสถาบันการเงินและ startup ด้าน Fintech ที่จดทะเบียนในไทยต้องเข้าร่วมการทดสอบความปลอดภัยด้านนวัตกรรมสนับสนุนบริการทางการเงิน (Regulatory Sandbox) ของธนาคารแห่งประเทศไทย ที่เริ่มขึ้นในไตรมาส 1 ปี 2017 ระยะเวลา 1 ปี ซึ่งไม่เพียงเป็นการส่งเสริมนวัตกรรมทางการเงิน และศึกษาผลกระทบที่อาจเกิดขึ้นแก่ภาคสถาบันการเงินในประเทศ แต่ยังคุ้มครองความปลอดภัยแก่ผู้ใช้งาน ซึ่งเป็นโอกาสให้นักลงทุนทั่วไปได้ทำความเข้าใจในบริการด้านเทคโนโลยีทางการเงินต่างๆ รวมถึง Robo advisor ก่อนเริ่มใช้งานจริง

· อีไอซีมอง Robo advisor เป็นโอกาสเสริมคุณภาพบริการแนะนำการลงทุนของสถาบันการเงิน โดยมองการสร้างความร่วมมือกับผู้ให้บริการด้านเทคโนโลยีดังกล่าวเป็นทางเลือกหนึ่งของสถาบันการเงินในการรักษา หรือขยายส่วนแบ่งตลาดในธุรกิจแนะนำการลงทุน เนื่องจากสถาบันการเงินมีความพร้อมด้านเงินลงทุนแต่มีแนวโน้มขาดความคล่องตัว และความชำนาญในการพัฒนาเทคโนโลยีดังกล่าวขึ้นมาใช้เอง ทั้งนี้ ในปัจจุบัน แม้ Robo advisor จะมีศักยภาพด้านการวิเคราะห์ด้วยตรรกะที่ดี แต่ยังต้องพัฒนาเรื่องความสามารถในการเชื่อมโยงข้อมูลที่ซับซ้อนเกี่ยวกับตัวผู้ใช้งาน รวมถึงความยืดหยุ่นในการสร้างปฏิสัมพันธ์กับมนุษย์ ดังนั้น การนำมาใช้ร่วมกับผู้ให้คำแนะนำด้านการลงทุน และบริการที่เกี่ยวข้องจึงเป็นโอกาสต่อยอดคุณภาพการให้บริการดังกล่าว

+++++++++++++++++++++++++++++++++++++++++++++

Robo advisors, the business opportunity that will transform the financial sector

· Robo advisors are Fintech applications designed to provide personal wealth management services online to general investors. Their selling point is their low cost as well as their capacity to develop into a provider of more comprehensive services similar to those offered by financial institutions.

· EIC see Robo advisors as an opportunity for financial institutions to enhance the quality of their personal wealth management services. This technology will improve service efficiency, which in turn will help financial institutions maintain and expand market share.

Robo advisors offer personal investment advice to ordinary investors by combining investment management, financial advisory and financial planning into a single wealth management service package. Such services previously targeted high net worth customers, making access difficult for those of more modest means. To cater to this under-served market, start-up businesses began developing robotic technology that used algorithms, big data management, and artificial intelligence integrated with financial advisory to formulate financial investment plans. These types of innovations in personal financial advisory are known as Robo advisors.

Robo advisors, which will tap the majority of diversified investors, are a Fintech closely watched by the finance industry around the world. Robo advisors were developed to replace face-to-face advisory in order to lower investment and wealth management advisory services costs for ordinary investors. The investment advice they provide is formulated on; 1) investment objectives, such as financial retirement planning or investment to raise wealth, and 2) investor risk appetites. Additionally, Robo advisors can adjust portfolios automatically to mitigate risk as well as provide other more comprehensive service functions such as tax loss harvesting, trading of fraction shares and margin loans to customers in the US . More premium services are also being provided by firms like Betterment and Schwab IP, offering personal investment advisory targeting high net worth individuals wanting to use this technology.

There are three key factors driving the widespread success of Robo advisors overseas. 1) Smaller initial investment requirement. Most investors previously did not have access to traditional advisory due a minimum investment barrier requiring 50,000 US dollars or more. However, some Robo advisor services, such as those provided by Betterment and Acom, have no set minimum balance. 2) Cheaper annual service fees. Robo advisors bring the average charge down to 0.0.5% of the asset under management compared to traditional service providers that charge a fee of 1-3% with other add-ons . 3) Investment advice can be accessed efficiently and personally online . In fact, Robo advisor providers like Wealthfront and Asset builder recommend a specific investment proportion of various financial products , factors that have led Robo advisors to becoming a prevalent solution in financial advisory to investors abroad.

Large financial institutions in the global market will maintain their major holding of the investment and wealth management advisory market share despite an expanding market for Robo advisors among startup businesses. Business Insider Intelligence, a business research unit, estimates that the value of Robo advisor businesses around the world will grow to 8 trillion US dollar by the year 2020, equivalent to 8% of the value of assets under management by financial institutions around the world . This shows that Robo advisors will have greater influence over the financial sector going forward. The top two leaders in Robo advisory, Vanguard PA and Charles Schwab, account for 74% of total assets under management among the top 10 firms, demonstrating that Robo advisors rely on firms that have the substantial capital necessary to develop the technology, a large customer base, a good reputation, and offering access to a broad selection of investment products.

Although Robo advisors are currently still under development, their service quality can be improved with the collaboration of involved businesses. Robo advisors manage a large pool of information and process data from multiple sources simultaneously in order to configure optimal investment choices. Nevertheless, Robo advisors still depend on human intervention, such as when trading financial assets that need to go through an agent, fund manager assessment of system performance, or when providing analysis and providing investment advice in complicated scenarios involving financial status, employment, and financial stability. Furthermore, given their limitation in helping firms build personal relationships with clients, which requires psychological and persuasive skills, Robo advisors should be used in conjunction with investment advisors or businesses related to wealth management and investment advisory to improve service quality.

General investors in Thailand are keen to invest with Robo advisors. Individual investors are more likely to rely on online services for their investment transactions going forward, in particular the online trading of assets, which has already risen by 30%. A survey by management consulting firm Accenture found that up to 94% of Thais surveyed are using online banking and are ready to use a Robo advisor to manage their investments. However, the technology is still largely unknown or is still limited to high net worth individuals.

Robo advisor providers in Thailand will need to pass the regulatory sandbox before starting business. Financial institutions and Fintech start-ups registered in Thailand will need to pass the financial innovation safety test of the Bank of Thailand starting from the first quarter in 2017, for a duration of one year. The safety framework not only supports financial innovations and helps form an understanding of their impact on the country's financial sector, it also ensures safety to users by allowing time for investors to learn about new financial service technology like Robo advisors before using the service.

· EIC sees Robo advisors as an opportunity to enhance financial advisory services provided by financial institutions. This type of collaboration with technology service providers offers an alternative strategy to help financial institutions maintain market share or expand their market in services related to investment advisory. This is because financial institutions have the readiness in terms of capital but are losing efficiency in doing business and lack the expertise in technology development. Even so, further developments of Robo advisors are still needed in regards to integrating more sophisticated data from users and increasing system flexibility to enable user interaction, whilst maintaining sound analytical logic. Taking into account the above, traditional investment advisory businesses and related services should take advantage of this technology to improve the quality of their services.